The Shoebox Full of Proof: When Americans Settled Every Debt With Ink and Paper

The Receipt That Could Save Your Life

Tuck away in millions of American attics, there are shoeboxes and manila envelopes stuffed with scraps of paper that once represented financial survival. Handwritten rent receipts. Scrawled IOUs. Careful ledger entries documenting every nickel borrowed and repaid. For most of American history, these pieces of paper weren't just records—they were legal armor that protected ordinary people from financial ruin.

Every transaction, no matter how small, generated a paper trail that both parties guarded carefully. Lose your receipt, and you might pay twice. Lose your ledger, and years of careful credit building could vanish overnight.

When Your Handwriting Was Your Legal Signature

Before computers standardized everything, the way you formed your letters carried legal weight that seems almost mystical today. Banks employed handwriting experts who could identify forgeries by the slant of an "S" or the loop of a "G." Your penmanship wasn't just personal style—it was biometric identification that courts recognized and criminals tried to copy.

Landlords, shopkeepers, and neighbors all developed the ability to recognize authentic signatures and detect suspicious alterations. A receipt written in obviously different handwriting could be challenged in court, making forgery a risky proposition that required genuine skill rather than digital manipulation.

This system created an informal network of document authentication that operated entirely through human observation and memory. People knew each other's writing styles the way we now recognize voices or faces.

The Neighborhood Ledger System

Corner stores, barbershops, and local services operated on credit systems that existed entirely in handwritten ledgers. The grocer kept a book with your family's name at the top of a page, recording every purchase, every payment, and the running balance in between. These weren't formal loans—they were community agreements based on reputation and relationship.

Customers could review their accounts anytime, challenging entries they disagreed with and watching the arithmetic that determined their standing. Both parties signed or initialed disputed items, creating a collaborative record-keeping system that required ongoing attention and mutual verification.

When families moved or businesses changed hands, these ledgers transferred like property deeds, carrying forward years of financial history and community relationships. Your grandmother's punctual payments could improve your own credit worthiness with the new owner.

Witnessed Agreements That Held Up in Court

For larger transactions—land sales, equipment purchases, significant loans—Americans relied on witnessed agreements that carried legal weight precisely because they were personal and local. Three signatures on a handwritten contract, especially if the witnesses were respected community members, could be more legally binding than formal documents notarized by strangers.

These agreements often included specific local details that made forgery nearly impossible: references to particular landmarks, family relationships, and community events that only genuine participants would know. A contract mentioning "the oak tree by Miller's barn where the church picnic was held" contained authentication details that no outsider could fabricate convincingly.

Photo: Miller's barn, via www.woodburymillerbarn.org

Photo: Miller's barn, via www.woodburymillerbarn.org

Witnesses took their responsibility seriously, understanding that their own reputation depended on the accuracy of their testimony. Being asked to witness a financial agreement was both an honor and a burden that connected individual transactions to broader community accountability.

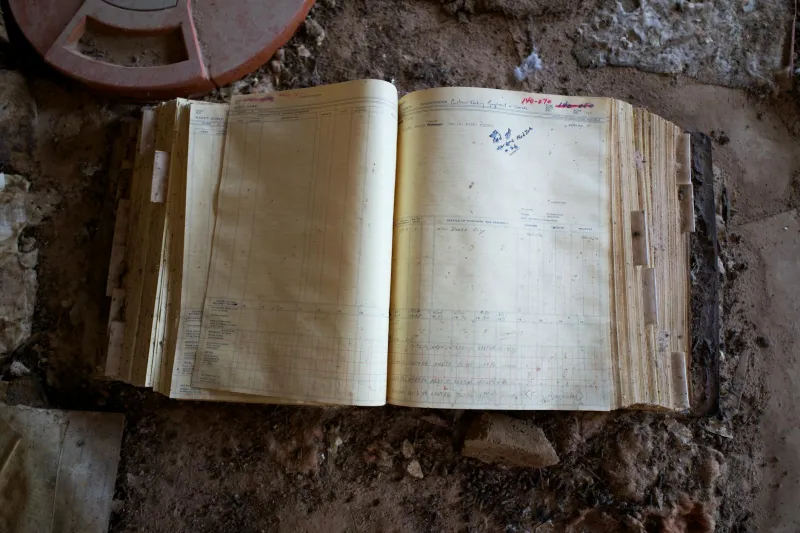

The Receipt Book That Ruled Everything

Rent payments, utility bills, loan installments—every regular financial obligation generated a steady stream of handwritten receipts that tenants and borrowers preserved like legal documents. Landlords used carbon paper to create duplicate receipts, keeping one copy and giving the other to the tenant as proof of payment.

These receipt books became the primary evidence in countless legal disputes. A tenant with complete payment records could fight eviction attempts. A borrower with proper documentation could prove loan terms that predatory lenders tried to alter. The paper trail wasn't just convenient—it was essential legal protection.

Families developed elaborate filing systems to preserve these documents, often organizing them by year, creditor, or transaction type. Losing receipts could mean paying debts twice or losing legal disputes that hinged on proving payment history.

When Math Errors Had Human Consequences

Every calculation was done by hand, creating opportunities for honest mistakes and deliberate manipulation that required constant vigilance. Addition errors in ledgers could compound over months, creating significant discrepancies that had to be resolved through negotiation rather than digital correction.

Both creditors and debtors learned to check arithmetic carefully, often performing the same calculations multiple times to ensure accuracy. Disputed totals led to line-by-line reviews that could take hours, with both parties working through the math together until they reached agreement.

This collaborative error-checking created a level of financial transparency that's hard to imagine today. Every number was visible, every calculation could be verified, and both parties understood exactly how balances were determined.

The Shoebox Archive That Proved Everything

American families became obsessive record-keepers by necessity, maintaining personal archives that documented every significant financial transaction. These collections weren't just organized chaos—they were carefully maintained legal resources that families consulted regularly and preserved across generations.

Estate settlements required surviving family members to reconstruct financial relationships using these paper records. Debts had to be verified, assets had to be documented, and obligations had to be honored based entirely on handwritten evidence that might span decades.

The physical nature of these records made them both vulnerable and valuable. Fire, flood, or simple misplacement could destroy years of financial history, while complete records could resolve disputes and protect inheritance rights.

What Disappeared With Digital Everything

Today's electronic transactions create perfect records that are simultaneously more accurate and less personal than the handwritten systems they replaced. We gained efficiency and lost the community relationships that once made financial agreements as much about trust as about money.

The paper trail that once connected every transaction to specific people, places, and relationships has been replaced by digital records that are more secure but less human. We can retrieve any transaction instantly, but we've lost the collaborative record-keeping that once made financial agreements a form of ongoing community conversation.

The transformation reveals how much of our financial system once depended on personal relationships, human memory, and the simple but powerful legal weight of ink on paper—a world where your word was literally only as good as your willingness to put it in writing, and where the shoebox under your bed might be the most important legal document you owned.